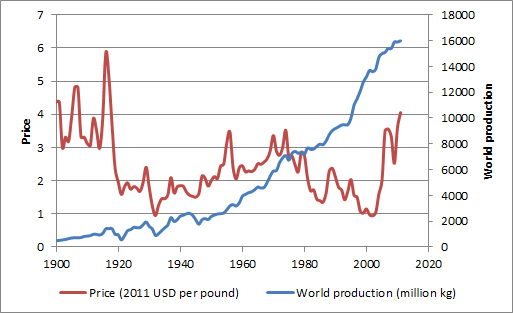

As we are only interested in change metrics (not necessarily the absolute values themselves), we bravely chose to take change of world production as a substitute for world consumption, thereby ignoring changes in recycling rates and stock levels. The data looks as follows:

Looking at the annual changes is more interesting to establish any relationship whether copper is a good indicator of consumption. this looks as follows (each dot represents a calendar year):

Ten year rolling correlation coefficient (and R2) looks as follows:

Our conclusions are as follows:

- Until 1980, Copper price was largely demand driven, with higher demand driving up copper prices. Production seemingly matched consumption or the changes to recycling rates and stock levels were not material enough to distort the picture.

- Since 1980 but especially for the last 15 years, the situation has become much more distorted, while volatility of world production (on a percentage basis) is at its lowest level since 1900, price volatility is at its maximum.

- Accordingly higher prices have recently not translated in higher production. At this stage of the analysis, it remains open to us what the underlying reasons are

We have also looked at the question whether copper price to copper production relationship is of lagging, concurrent or leading nature. The data suggested concurrent, but given that we have worked with annual data points we may need to refine this with monthly or quarterly data.